지은이: L. Randall Wray

출처: WORKSHOP-Understanding Unemployment in Australia, Japan and the USA: A Cross Country Analysis, 10 and 11 December 2001, Centre for Full Employment and Equity, The University of Newcastle, Australia.

In my recent book (Wray 1998), I attempted to explain how a modern monetary system works through revival and extension of the old Chartalist or State Money approach endorsed by Keynes and best exposited by Knapp. My book has since been the subject of several reviews (Lavoie, Mehrling, Niggle, Togati, Rossi) and related ideas were examined in several articles (Kadmos and O'Hara, Dalziel, Lavoie, Aspromourgos, Danby, Davidson). The approach has been variously dubbed "neo-Chartalist" or "taxes-drive-money" (TDM).

In this article I intend to correct some errors of interpretation while clarifying and extending some of the issues. Due to space constraints, I will limit the focus of this article to theoretical issues, leaving to the side related policy issues except where it is absolutely necessary to introduce them. ( ... )

1. What is money?

Defining money is a constantly vexing problem for monetary theorists. Readers are quite familiar with the two usual approachesㅡ

defining money by its functions (the textbook approach),

or by simply and arbitrarily choosing some empirical definition (as Keynes did in the

GT: “we can draw the line between ‘money’ and ‘debts’ at whatever point is most convenient”, Keynes 1964 p. 167

{ㄱ}). However the critical distinction that must be made is between

money as a unit of account and

money as a thing that is denominated in a unit of account (as did Keynes in the ^Treatise^: “the money-of-account is the description or title and the money is the thing which answers to the description”, Keynes 1930, p. 3

{ㄴ}). Most theorists, and several of my reviewers (most notably, Mehrling) makes no such distinction and thereby become entangled in a morass of confusion as they use the term money to sometimes refer to the "thing" and other times to refer to the "title" (reminiscent of the mistake Keynes identified: "like confusing a theatre ticket with the performance", Keynes 1983, p. 402

{ㄷ}). In order to avoid adding to the confusion, throughout this articel, I will carefully distinguish among 'money' (the 'title, or dollar in the US), high powered money (HPM, a particular money thingㅡreserves and currency, or what I confusingly called fiat money in the book), and bank money (another money thingㅡdemand deposits or private bank notes). When I use the term money without a qualifier, I mean the unit of account; in the case of the US, "money" (without qualifier) is the dollar; in the UK, it is the pound.

- CF{ㄱ} General Theory, Chapter 13, footnote no.1.

- CF{ㄴ} Treatise on Money, Chapter 1.

- CF{ㄷ} Keynes(1914a) says:

“[Friedrich Benedixen says that the] old 'metallist' view of money is superstitious, and Dr Benedixen trounces it with the vigour of a convert. Money is the creation of the State; it is not true to say that gold is international currency, for international contracts are never made in terms of gold, but always in terms of some national monetary unit; there is no essential or important distinction between notes and metallic money; money is the measure of value, but to regard it as having value itself is a relic of the view that the value of money is regulated by the value of the substance of which it is made, and is like confusing a theatre ticket with the performance. With the exception of the last, the only true interpretation of which is purely dialectical, these ideas are undoubtedly of the right complexion. It is probably true that the old 'metallist' view and the theories of regulation of note issue based on it do greatly stand in the way of currency reform, whether we are thinking of economy and elasticity or of a change in the standard; and a gospel which can be made the basis of a crusade on these lines is likely to be vary useful to the world, whatever its crudities or terminology.”(Keynes 1914a: 418) ─“Theorie des Geldes und der Umlaufsmittel by Ludwig von Mises; Geld und Kapital by Friedrich Bendixen”(review), Economic Journal 24.95 (Sep.): 417–419. From a blog.

In my view, money is not simply a handy numeraire in which prices, debts, contracts (or, indeed, HPM and bank money) happen to be denominated. My approach can thus be contrasted with, say, a GE approach, in which we may choose any one good to serve as numeraire, converting relative values to nominal values. Indeed, the typical story of the origins of money is really based on a numeraire approach, in which Robinson Crusoe decides to use "tobacco, leather and furs, olive oil, beer or spirits, slaves or wives. ... huge rocks and landmarks, and cigarette butts" as "money". (Samuelson 1973, pp. 275-6) When, say, seashells are chosen as money by Crusoe, he has simultaneously chosen a numeraire and designated what will serve as the money-thing. Similarly, the orthodox account of the gold standard conflates the money-thing with the money-description (unit of account). It is only later in the story that the goldsmith succeeds in blurring the line between the object and the numeraire by issuing circulating receipts backed by gold. And we do not really achieve complete separation, and thus, a pure unit of account until the evil government comes along with a fiat money. A sharp distinction is thus made between a "commodity money"ㅡwhich is nothing but a GE numeraireㅡand a fiat money denominated in a unit of account. In my view, this is the wrong distinction that results from conflating money with the money-thing. (See also Heinsohn and Steiger 2000, p. 97.)

Unfortunately, Mehrling proposes an equally unhelpful distinction, originally advanced by Schumpeter as a credit theory of money versus a monetary theory of credit. In Mehrling's hands, this becomes "fiat money" versus "credit". By fiat money, Mehrling appears to means nonconvertible money-things issued by government; by credit he appears to mean nonconvertible money-things issued by private entities. Further, he seems to believe that my own theory is of a "modern money" system based on "fiat money", so defined, and is contrasted with his own theory of a "modern money" system based on "credit", so defined. Actually, my approach is a neo-Chartalist or State money, or taxes-drive-money, approach and applies to any monetary system in which the state determines the unit of account in which the money-things are denominated (whether these are "fiat money" or "credit"). Certainly there are differences between what Mehrling calls "fiat money" and "credit", however, both these money-things are issued into a "modern money" or "chartal" or "state money"

system. As Keynes argued, the state money system has existed "for some 4000 years at least", beginning when the state claimed the right to name the money, as well as "the right to determine and declare what thing corresponds to the name, and to vary its declaration from time to timeㅡwhen, that is to say, it claims the right to re-edit the dictionary". (Keynes 1930, p. 4) While we can easily imagine a state money system that operates only with "credit" money-things, in point of fact all existing nation states actually issue some of the money-things. Because Mehrling conflates money-things with money, he fails to recognize the important characteristics of a state money system. The important distinction to be made is between a system in which the state designates the unit of account, versus the (probably only imaginary) system based on a numeraire that might have evolved out of some competitive market process. (Klein and Selgin 2000) Mehrling's "credit money" can exist in either sort of system. However, in all modern state money systems, there is a hierarchy of money-things and it is no coincidence that HPM (or "fiat" money-things) sits at the top.

In this article I want to avoid historical debate as much as possible, but I will assert that the conjectural history propagated by Samuelson (and others, and apparently mostly believed by some of the reviewers) is dismissed by

all serious historians and anthropologists. Interested readers are referred to accounts

(Cook 1958

; Crawford 1970

; Davies 1997

; Goodhart 1998

; Grierson 1965, 1977, 1979

; Heinsohn and Steiger 1983

; Hoppe and Langton 1994

; Hudson 1998

; Ingham 2000

; Kraay 1964

; Kurke 1999

; Magubane 1979

; McIntosh 1988

; Neale 1976

; Redish 1978

; Rodney 1974

; Zarlenga) that emphasize the social nature of the origins of money, including the role played by the precursor of the modern state.

What I wish to do is to call attention to the substantial logical problems entailed in the typical approach taken by economists. So far as I know, there are only two lines of research that attempt to derive a numeraire from private maximizing behavior.

[:]

- The first is the Austrian school, which supposes that an evolutionary process could have selected for the transactions-cost-minimizing medium of exchange. (Parguez 2000, Klein and Selgin 2000, Dowd 2000, Wray 2000) However, it is widely recognized by the Austrians, themselves, that no satisfactory exposition yet exists.

- The second, more fruitful, approach is that taken by Heinsohn and Steiger (1983; and also adopted in Wray 1990, and updated in Heinsohn and Steiger 2000) that traces development of the unit of account from private loans of grain. I now view this as a satisfactory explanation of the origins of private credit (money-things) denominated in a pre-existing social unit of account, however, I believe it still suffers from logical problems involved in hypothesizing a spontaneous choice of a universal unit in which debts would be denominated. Further, I fear it hypothecates a later societal form of organization to the distant past. I believe it is unlikely that an economy based on private ownership of productive land pre-existed civilization and its accoutementsㅡwriting, money, and rudimentary "state". While we all know and love the Lockeian story of the origins of private property, it is fanciful at best. (Henry 1999)

In any case, the primary purpose for examining history and pseudo-history is to shed light on the nature of modern money.

- In my view, a system based on a commodity money is not a "money economy" as Keynes defined it. Rather the commodity money economy is an (imagined) economy in which money serves as nothing more than a numeraire; it is what Keynes called a non-money or barter or real wage economy.

- Thus, even if there really has been a historical stage in which there was a commodity (numeraire) money, I would argue that it sheds no light on the operation of our modern money system (and recall that Keynes argued that the modern money system is at least 4000 years old).

The useful dichotomization of theory is that between what Goodhart (1998) has called C-form (Chartalist) and M-form (Metalist, or commodity money)ㅡthat is to say, between a system in which money is a social unit of account or that in which money is nothing more than a numeraire adopted for convenience.

The State theory, or taxes-drive-money (TDM), or neo-Chartalist approach insists that the state “writes the dictionary” in all modern economies. This goes a long way toward explaining what would appear to be

an otherwise extraordinary coincidence: the one-nation-one-currency rule. As Mundell's work makes clear, if money is simply a numeraire chosen to facilitate exchange, then one would expect use of a particular numeraire within an ‘optimal currency area’. (Mundell, Goodhart) There is no reason to expect such to be coincident with nation states.

In fact, however, the one-nation-one-currency rule is violated so rarely it borders on complete insignificance. Further, those few cases are easily explained away as special cases, as Goodhart demonstrates.

Finally, a word about the Post Keynesian preoccupation with the link between uncertainty and the use of money. It is often argued that money is used BECAUSE the future is uncertain. However, it is normally recognized that the future in a monetary economy is uncertain in a very particular way. That is, the individual in a monetary economy is mainly concerned with uncertainty about nominal things: nominal inflows and outflows, nominal prices, values of nominal wealth, future nominal interest rates. These uncertainties exist only in money-using economies (and, tellingly, do not exist in GE models that use money only to facilitate exchange). It would be thus rather circular to argue that we use money to protect us from a kind of uncertainly that exists only in a money-using economy. Given organization of production around money (that is, a monetary production economy) use of money may well reduce individual uncertainty (even as it raises society's uncertainty), but this cannot explain the origins of money. Acknowledgment of existence of this particular kind of uncertainty, thus, sheds little light on the NATURE of money, nor, ultimately, on the USE of money.

I do, however, agree with Davidson's (2001) argument that given uncertainty and use of money, use of enforceable monetary contracts is a viable means of reducing uncertainty. Davidson also recognizes, as did Keynes, that "in a 'cooperative economy' where all parties trusted all other parties, there would be no need for money as we know it", while in "a market economy", most buyers and sellers do not have such familiar, trustworthy relationships." (Davidson 2001, p. 425) In such entrepreneurial economies, "state enforcement of voluntary obligations if either party reneges is a necessary condition for a monetary economy ..." (ibid) Danby (2001) labels Davidson's approach "contractual chartalist", as opposed to my "tax-based chartalist", because the primary role of the state in Davidson's view is to enforce private monetary contracts. However, I do not deny the practical importance of state enforcement, nor do I deny the significant role played by such contracts and enforcement in reducing individual insecurity. I simply insist that one cannot logically derive the origins of money from such concerns.

2. Taxes Drive Money

This leads us to an explanation of the use of money: why is money used? My dissertation advisor, Hyman Minsky, continually warned me against rewriting

Genesis, good advice that I've been ignoring for almost two decades. The orthodox story of

Genesis, begins, as we've seen, with the Garden of Eden and Crusoe and Friday who grow tired of the inconveniences of barter. In any case, money comes out of the market. In the Heinsohn and Steiger version, it derives from private loans of property (a view apparently favored by Mehrling). The shared understanding of each of these is a non- or even anti-social methodological individualism (Danby 2000; Parguez 2000; Ingham 2000) Such methodology is clearly antithetical to the approach taken by most heterodox economists, and in particular by institutionalists, social economists, and Marxists. Post Keynesians appear to be more willing to adopt methodological individualism, for reasons beyond the scope of this article. However, there is a tradition even within Post Keynesian thought that embraces a cultural, anthropological, social approach to money (

Danby 2000; Davidson 2000; Ingham 2000).

For the record, I believe that money derived out of the pre-civilized practice of

wergild; or to put it more simply, money originated not from a pre-money market system but rather from the

penal system.[n1] (

Grierson 1977; Goodhart 1998)

[:]

- An elaborate system of fines for transgressions was developed in tribal society.

- Over time, authorities transformed this system of fines paid to victims for crimes to a system that generated payments to the state. (Innes 1932)

[n1] Hudson (2001) has developed an alternative thesis for the origins of the money of account in Babylonia. Rather than locating the origins in wergild, he argues it was created within the temple and palace communities for internal accounting purposes. Clearly, however, his argument also focuses on the social nature of the origins.

Until recently, fines made up a large part of the revenues of all states. (

Maddox 1769) Gradually,

fees and

taxes as well as

rents and

interest were added to the list of payments that had to be made to authority. To be clear, I do not imagine an all-powerful state (as Mehrling implies),

but rather a gradually evolving institution that at times was more, and less, accepted as a legitimate authority and that was more, and less, operated on democratic principles. All that is necessary is to posit that

some sort of authority exists that can levy obligations on a populationㅡanything from fines or tithes to fees and taxes. Such an authority can range from a powerful Egyptian pharo to a beleaguered Greek city state trying to wrest power away from an elite (

Kurke 1999), to a weak English crown, and from a fascist 1930s era government to a new millennium democratically elected representative form of government in which a supreme court intervenes to award the presidency to a previous ruler's electorally-challenged scion.

Thus, when the neochartalist approach is identified as TDM, this is not meant to narrowly limit the scope to the special case of, say, ability to impose high income taxes by some authoritarian 1984-ish state. Quite the contrary. All that is required is an ability to

create and impose an obligationㅡthe exact nature of which is defined by the authorityㅡno matter how weak that authority might otherwise be.[n2] Whether this obligation take the form of payment of a tithe (the penalty for nonpayment of which is believed to be eternal damnation), a fine for activities that are mostly unavoidable (say, hunting deer in the king's forest to obtain protein needed for survival), or a head tax (required to maintain one's head on one's shoulders) is rather immaterial.

[n2] Kregel has pointed out to me that English kings were very inventive in creating all sorts of obligations imposed on their subjects. He emphasizes that we would not have patents or corporate charters without these clever inventions of rights to the fruits of such imposed obligations.

The TDM approach has quite wrongly been characterized as narrowly applying only to income taxes. In fact, income taxes alone cannot possibly explain the genesis of money for the obvious reason that an income tax would have been entirely avoided by not earning money-denominated income. The key is the unavoidable nature of the obligiation, and the head tax is probably the best motivating device knownㅡas was well understood by Africa's colonizers. (Rodney 1976) This does not mean it is essential that no one can ever avoid the obligationㅡsome have always escaped the gallows, others have not felt constrained by the threat of life in hell. Nor is it necessary to impose this obligation on all members of society. Even if only a small percent of society can be compelled to feel it necessary to "pay up", such obligations can monetize an economy and move resources to authorities. Apparently, a significant portion of the population still feels it necessary to pay the 'obligatory' tithes to religious institutions to keep the clergy rich in the finer objects of life. Still, the threat that the IRS will tap wages and confiscate assets seems to serve as a more efficient motivating device than the threat of eternal damnation. And one suspects that, as I argued in my 1990 book, creation of modern democratic government and belief in social obligations has proven to be evolutionarily superior to any other system; after all, the tithes is only 10% of income, but highly democratic states in societies with high development of feelings of social responsibility have at times been able to achieve marginal tax rates as high as 90%. (It is telling in the US today, the sense of social obligation has deteriorated sufficiently that our President can proclaim that no one should feel obligated to pay more than 33% of her marginal income to the federal government.)

What do we mean by TDM? We mean that

[:]

- the "state" (or any other authority able to impose an obligationㅡwhether that authority autocratic, democratic, or divine) imposes an obligation in the form of a generalized, social unit of accountㅡa moneyㅡused for measuring the obligation.

- The important step, then, consists of movement from a specific obligationㅡsay, an hour of labor or a spring lamb that must be deliveredㅡto a money obligation.

- This does not require the pre-existence of markets. Once the authorities can levy such an obligation, they can then name exactly what can be delivered to fulfill this obligation. They do this by denominating those things that can be delivered, in other words, by pricing them. To do this, they must "define" or "name" the unit of account.[n3]

This resolves the conundrum faced by methodological individualists like the Austrians and some Post Keynesiansㅡonce we have a unit of account and a price we can finally have a numeraire without a spontaneous virgin birth.[n4]

[n3] As Keynes argued, "A money of account comes into existence aling with debts. ... and price lists" (Keynes 1930 p. 3); it is clear that the monetary obligation imposed by the authority is the important debts so far as my approach is concerned, although Keynes was using the term more broadly).

[n4] Mehrling cites Braudel's workㅡon 13th~15th century Europeㅡas evidence against Chartalist speculation on the history of money. However, the origins of money lie deep in the distant pastㅡ3000 or maybe 10000 years before medieval Europe. Others hint that the State theory of money cannot apply to the case of the US before 1913, because before that date we did not have a central bank; others link the TDM view to an income tax, arguing that since the US did not have an income tax before WWI, the TDM approach cannot be applied to the US before that date. All of these arguments are spurious. Even if a country only had a customs house and a tariff on necessary imports, this can "drive" money.

3. The Gold Standard and State Money Things

Thus far we have only explained the money of account (the description). Once the state has named the unit of account, and imposed an obligation in that account, it is free to choose “the thing” that “answers to the description”. It could, for example, say that it will accept 27 grains of gold in payment of one unit of tax obligation. By doing so, it has

monetized gold,

rendering it a “money-thing” (gold money) denominated in the unit of account.

- Note that even if gold is the only money-thing that answers to the description, gold is not merely a conveniently chosen numeraire, one good among many chosen by acclamation of individual barterers. Rather the state must denominate gold in its unit of accountㅡthe unit in which taxes are denominated.

- Note, also that the state can make anything it wants answer to the description, and, as Knapp emphasized, can change "the thing" any time it likes: "Validity by proclamation is not bound to any material" and the material can be change to any other so long as the state announces a conversion rate (say, so many grains of gold for so many ounces of silver). (Knapp 1924, p. 30)

The State money stage begins with the state writing the dictionary and naming the thing that answers to the description; the modern money stage is fully achieved when the state actually issues the money-thing answering to the description it has providedㅡthat is, HPM. Economists often distinguishe between a "commodity money" (say, a gold coin) and a "fiat" paper money. However, in my view, the material from which the money thing issued by the state is produced does not matter (at least in determining the nominal value of the money thing)ㅡin both cases, the state must announce the nominal value of the money thing it has issued (that is to say, the value at which the money-thing is accepted in meeting obligaions to the state).

It is frequently argued that a gold standard is an example of a commodity money system. However, it is actually a state money system in which the state denominates gold in the money of account; and it is a modern money system so long as the state issues the gold money thing accepted in payment of taxesㅡtypically gold coins or notes issued against warehoused gold. The state might limit its own spending to the quantity of gold it can obtain (either directlu coining the gold, or issuing redeemable notes against gold held on reserves) at a fixed rate of nominal spending against its gold.[n5] Because the states's spending is then limited to the quantity of gold it can obtain, it will almost certainly require gold (or gold-backed notes) in payment of taxes. The populatioin will have to obtain gold from the state's spending, from domestic mining activity, from abroad, or by melting down jewelry and other valuables. As conventionl theory makes clear, interest rates will tend to be endogenously determinedㅡwhen a nation faces a gold drain, it can raise interest rates to try to reverse gold flows. If a nation does not maintain a full bodies gold-money but rather adopts a fractional reserve, it must always worry that it cannot convert all outstanding money-things to the gold-money. Hence its interest rates is endogenous and spending by state (though emission of money-things) is constrained. As we will discuss below, it is not the material from which gold money is manufactured, but rather the fixed exchange rate against a relatively scarce commodity that is significant. This the rel import of a gold standardㅡnot because it is "alchemistically" turns gold into money (reversing Mehrling's characterization) but rather because it ties the hands of the state and endogenizes the interest rate.

[n5] A gold standard in which the state picks an arbitrary reserve ratio of gold to be held against notesㅡsay 25% gold backing against notes issuedㅡbut in which the notes are irredeemable may not actually tie the hands of government at all if it is free to change the reserve ratio any time it likes. The following discussion does not apply to this sort of system.

However, in spite of the amount of ink spilled about the gold standard, it was actually in place for only a relatively brief instant.

- Typically, the money-thing issued by the authorities was not gold-money nor was there any promise to convert the money-thing to gold (or any other valuable commodity).

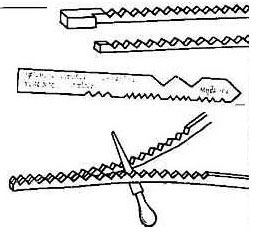

- Indeed, throughout most of Europe's history, the money-thing issued by the state was the hazelwood tally stick. Other money-things included clay tablets, leather and base metal coins, and paper certificates.

- Why would the population accept otherwise "worthless" sticks, clay, base metal, leather, or paper? Because the state agreed to accept the same "worthless" items in payment of obligations to the state.

Knapp distinguished between

“definitive” money accepted

by the state in ('epicentric') payments of obligations

to the state, and

“valuta” money that is the money-thing used

by the state in its own payments ('apocentric').

- In today's modern money systems, HPM fulfills both functions. Of course, it appears that the US government accepts bank money (demand deposits) in payment of taxes, but in reality payment of taxes by bank check leads to a reserve drain from the banking system. Government spending normally takes the form of a treasury check, which when deposited leads to a reserve credit. Note that so long as government does accept bank money in epicentric payments at par with high powered money, from the point of view of the nonbank public there is no essential difference between bank money and HPM. This is not true for banks, which lose reserves when taxes are paid by bank check and gain reserves whenever treasury checks clear.

- Finally, Knapp defined as 'paracentric' payments made between nongovernment entities. In all modern economies, these mostly involve use of bank money and other money-things issued by the non-governmental sector (what can be called "inside" or "credit" money as one prefers).

- There is of course a hierarchy or pyramid of money-things with non-banks mostly using bank liabilities for net clearing and with banks using HPM for net clearing with other banks and with the government (handled on the books of the central banks). Note that "monies" are denominated in the money of account, that is, the account in which obligations to the state are enumerated.

Once

[1] the state has created the unit of account and named that which can be delivered epicentrically to fulfill obligations to the state, it has generated the necessary pre-conditions for development of markets.

- All the evidence suggests that in the earliest stages the authorities provided a full price list, setting prices for each of the most important products. Once prices in money were established, it was a short leap to creation of markets.

- This stands orthodoxy on its head, by reversing the order: first money and prices, then markets and money-things (rather than barter-based markets and relative prices, and then numeraire money and nominal prices).

[2] The next step was the recognition by government that it did not have to rely on the mix of goods and services provided by taxpayers, but could issue the valuta money-thing to purchase the mix it desired in apocentric payments, then receive the same money thing (this time acting as definitive money) in the epicentric tax payments by subjects/citizens (in Keynes's terminology, this is the act of naming what thing answers to the description). This would further the development of markets because those with tax liabilities but without the goods and services government wished to buy would have to produce for market to obtain the means of paying obligations to the state. Again, this point was well-recognized by Africa's colonizersㅡimposition of monetary tax liabilities played a key role in monetizing Africa.

4. Money and Government Spending

Post Keynesians frequently argue that only money economies have unemployment, and sometimes identify uncertainty as the underlying cause of unemployment. Note that as we argued above, uncertainty cannot explain the origins of money, nor can it be the ultimate cause of unemployment. If the state imposes a tax liability and then lets its spending of the money-thing accepted in tax payments expand until all who wish to obtain the money-thing have been satisfied, there will be no unemployment even in a money economy (in the sense that anyone can provide goods or services to obtain the money thing from government). If however the state were to limit its spending below the level that would provide subjects/citizens with the means of tax payment desired, there could remain a 'queue' of those willing to 'work' to supply goods and services to government and/or markets, but unable to find a demand for their goods and services. They are effectively 'unemployed' because of insufficient government spendingㅡthe source of means of tax payment.[n6] Note also that this unemployment could exist even in the case of an 'ergodic' future. ( ... ... ) [n7]

[n6] Government restriction of supply of HPM is a necessary but not sufficient condition for the existence of unemployment. Even in the presence of government restriction, if private markets supplied enough work for all who want to work, full employment could be maintainedㅡat least for a while.

As mentioned above, there is a hierarchy of money-things in all modern economies. Usually, one uses liabilities higher in the pyramid to discharge one's won liabilities. But in any case, any private entity must use third party liabilities to discharge its own money-denominated liabilities.

The case of a state that imposes a tax obligation is quite different, however.

- When it spends by issuing the money-thing (valuta and definitive) accepted in dispensation of that obligation to pay taxes, the state does not need a third party liability to 'discharge' its own 'liabilities'.

- Indeed, while HPM is often said to be the 'debt' or 'liability' of government (central bank and treasury), it is not a liability in the normal sense of the term, for the government is not 'liable' to deliver anything to retire high powered money. When government issues HPM to buy something, it is 'liable' only to accept that same HPM in epicentric (i.e. tax) payments to the state.

- Thus, when Rossi argues, "As a matter of fact, it is plain that no agent whatsoever can really pay by acknowledging his/her debt to another agent. ... The emission of modern money is never a purchase for the issuer", he is clearly confusing the position of a user of HPM with that of the issuer. (Rossi p. 484) When the state issues HPM, the only sense in which government is 'in debt' to holders is that it must allow taxpayers to retire their obligations by delivering HPM. Once they have done so, the government is no longer 'liable' for anything.

- What Rossi and many others forget is that unlike a bank, the state creates and imposes a tax liability on its population,[n8] making the population liable to deliver any money-thing designated by the state as acceptable at state pay offices. It is true that no private agents can "buy" anything simply by issuing their own liabilities, for they would remain "indebted" by so doing.

- The apparent difference between a privately issued money-thing and the state's HPM money-thing lies not so much in the money-things themselves but rather in the different ability to impose money-denominated liabilities. This is the true source of sovereign power, and this is what puts the state's money thing at the top of the hierarchy. The relations in a "free market" economy that are based on "voluntary" money-denominated contracts do not give sovereign power to private entities. However, it is easy to find examples throughout history in which, say, a feudal lord or an owner of a company town is able to exercise sovereign power in its jurisdiction, and hence able to "buy" through issuing its own "liabilities".[n9]

[n8] Again, it may be necessary to note that I am not assuming an "all powerful" or fascist state. Even the most democratic forms of government "impose" tax obligationㅡeven if the taxpayers vote unanimously for such levies.

[n9] Government can, if it so chooses, attempt to tie its own handsㅡand thereby reduce its sovereigntyㅡby promising to redeem its HPM on demand for something elseㅡgold, foreign currencyㅡin which case it chooses to make itself "liable" for delivering such. See below.

Mehrling similarly paints a fancifyl, if not bizarre, picture in which government is nothing more than a large "ongoing business"ㅡperhaps a giant Microsoftㅡfrom which we buy "a variety of services". (Mehrling 2000, p. 402) Further, "we are all willing to extend credit to the government", temporarily accepting its liabilities because we will use these to buy its services. (Mehrling 2000, p. 402-403) Mehrling is obviously conflicted about this, however, adding a footnote recognizing "that government spending is not limited in any simple way by its ^current^ taxation". (Mehrling 2000, p. 402, n. 4; emphasis added) Lest we fear that he has retreated into some sort of Barro-Ricardian equivalents argument, he admits that government spending is not even limited by "the present value of all future expected taxes". (ibid.) What then determines willingness of the private sector to extend "credit" to government? Given his earlier discussion, one would expect it to be the discount flow of government services the public expects to purchase over the infinite horizon. But no, Mehrling finally concludes that willingness to accept HPM is a function of the state's "taxing authority" and the amount of "credit" the public will extend exceeds current taxes if there is "unused" taxing authority. In the final analysis, then, he merely accepts a convoluted version of the state money approach he wishes to criticize, substituting "unused taxing authority" for tax obligataions, and his vision of government as nothing but a large Microsoft that produces services for purchase proves to be nothing but a diversion.[n10]

If, as I have argued, HPM is accepted from inception because government first imposes a tax liability, then why will the private sector accept more than is required for immediate needs to fulfill obligation to government? The most obvious reason is that HPM is universally accepted as a medium of exchange and means of payment, hence, (a) one can purchase goods and serves (not just from government, but also from the private sector), (b) one can retire liabilities to nongovernment entities, and (c) one can hoard it for unspecified future use. Of course, (a) and (b) only shift it from pocket to pocket; ultimately all the HPM must be voluntarily held as net hoards for unspecified future use. In order for the nongovernment entities to net hoard HPM, government must provide more HPM than it drains through tax paymentㅡin other words, government must run a deficit.

What happens if the desire to net hoard HPM is zero? In that case, government would find that once the private sector has received all HPM it requires to pay taxes, government would offer HPM to buy goods and services, but would find no takes. (Or, incomes must rise until the desire to net hoard equals the government deficit.)

On the other hand, what if government's provision of HPM left an unsatisfied demand for HPM for hoarding? The government would see queues of those offering goods and services for sale for HPM. As we discussed above, this could be defined as unemployment, as there would be people willing to work to supply goods and services to obtain HPM.

Note the relation of this argument to Keynes's claim that unemployment results because people want the moonㅡliquidityㅡand that the solution is to operate a green cheese factor to meet the demand.

5. Financing Government Deficits

It is not quite so simple in our modern economy, of course, because for the most part HPM is used mostly for account clearing (plus illegal activities). There is little reason for nonbanks to hoard HPM if bank liabilities exchange, and are expected to continue to exchange, at par against HPM, and if bank money is accepted in tax payments. Hence, most of the time HPM will be held within the banking system. Under this arrangement, is there still a reason to expect a desire for net hoards of HPM? Yes, for two reasons. First, the banking system uses HPM for net clearing among banks and with the government, hence, one would expect to see a positive balance of HPM held as assets of the banking system. Of course, adding a reserve requirement ensures a legal imperative for positive balances, although banks would almost certainly desire some positive balance unless there exists a smoothly functions overdraft facilities through which government lends HPM required for clearing on demand.

The second reason to expect accumulation of HPM balances is a bit more complicated, and is related to the desired portfolio balance of the private sector. In a closed economy, all 'inside' financial wealth is offset by 'inside' debt, and the surpluses of some entities over any period are exactly offset by the deficits of other units.

{*} When government deficit-spends, this allows the private sector's income and wealth to increase without requiring any private entity to incur deficits or debt. Thus, government deficits can increase national income and allow net wealth to rise above zero. This may well encourage some private entities to increase spending, incurring deficits and inside debt, while at the same time encouraging other private entities to "surplus spend", taking up private sector inside debt. We would normally expect that the nongovernment sector will want to accumulate some outside, or net, wealth in the form of HPM, perhaps as a ratio to inside wealth, and/or as a ratio to income flows. Depending on the government's spending and taxing rules (Are taxes set as a percent of nongovernment income flows? Is spending countercyclical?), the size of the government deficit or surplus (hence the net quantity of HPM it injects or drains) may be endogenously determined by the nongovernment sectors' desire to "net save" in HPM.

CF{*} 중앙은행을 제외한 자금순환표 (중앙은행의 세 가지 통화정책)

However this is still too simple because thus far we have assumed government spends by emitting HPM, some of which is then drained in tax payments such that the outstanding stock of HPM depends on the budget surplus or deficit. However, in most modern economies, government issues government bonds equal to a significant portion of its deficit (or retires bonds as it runs surpluses). This means the private sector accumulates (or loses) some government bonds in addition to HPM. This is usually called 'government borrowing' and is thought to be necessitated by government deficits. This also brings up the issue of government payment of interest, thought to be required to enable government to "borrow" and deficit spend. Most orthodox and even may heterodox economists believe that the market dictates to government what interest rate it must pay: Mehrling goes so far as to claim government does not have "the ability to set ... the rate of interest as an exogenous policy datum", and while he admits that "the state borrows at the lowest rate of interest", he insists "its debt must compete with privately issued debt". (Mehrling 2000, p. 403) Similarly, Asmpromourgos gop[?] insists "the issuing of securities is an essential part of the complete process of effecting the rise in public expenditure" (Aspromourgos 149, see also 150-151). [n11]

[n11] He also says (Aspromourgos p. 151) that bond issue is essential to "funding", "or, if one prefers, 'sustaining', 'supporting' or 'effecting'", to come up with a way of avoiding the fact that since the deficit spending has occurred ^before^ the bond sales logically can take place, bond sales ^cannot^ have been required to allow the deficit spending to occur, or any normal use of the meaning of terms he uses or of interpretations of the concept of causation.

In my book, I called bond sales an 'interest rate maintenance operation', not a financing operation. The government does not 'need' to 'borrow' its own HPM in order to deficit spend. This becomes obvioius if one recognizes that government bond sales are logically impossible unless (a) there already exist some accumulated HPM with which the public can buy the government bonds, or (b) government lends HPM used by the public to buy the government bonds, or (c) government creates some other mechanism to ensure that sales of bonds to the public do not lead to a debit of bank reserves of HPM. Therefore, government bond sales cannot really 'finance' government deficits. This is recognized by most heterodox economists; even Aspromourgos admits "government expenditure is effect entirely by creation of injection of outside money" (Aspromourgos 149), however he then incongruously rejects the obvious conclusion that "tax and bonds do not 'finance' government expenditure". He does this by arguing that those who receive HPM may not wish to accumulate hoards of HPM, thus, government must sell government bonds to drain the 'excess or undesired liquidity'. (Aspromourgos p. 149; See also Dalziel 2000, who argues this "excess liquidity" can cause inflation.) While he weaves, dodges, and floats all around the point, never really telling us how the public forces government to sell government bonds "to restore a final or complete equilibrium position for all agents in the system", Aspromourgos does seem to vaguely recognize that it has something to do with "an interest-setting procedure" adopted by government. (Aspromourgos p. 149) Hence, while it is not clear exactly what he has in mind, he does not seem to accept Mehrling's belief that the government's bonds "compete" with private debt.

It is really quite simple. Government deficit spending generates hoards of HPM to satisfy the nongovernment sectors' desire to 'net save' in the form of non-interest earning HPM. The government could leave things there (as Japan does today), but might instead choose to pay a positive interest rate by draining some of the HPM through sale of interest earning government bonds. Clearly, government can set the interest rate anywhere it likes; rather than 'competing' with private debt, this will instead set the base rate below which private borrowers normally will not be able to borrow by issuing debt with similar maturity. While it is not at all necessary, government can issue debt with a wide range of maturities and then peg the interest rate on each of these. Normally, in the US, government only pegs the shorter bill rate. How does that work? In the US, the Fed announces a fed funds target and then supplies/drains reserves to keep just the amount of HPM in the system that is required by banks and the nonbank public, allowing the Fed to hit its overnight target. The Fed can always tell whether there is too much/too little HPM in the economy simply by watching the fed funds rate. If it moves above the range, the system wants to sell bonds to the Fed in order to obtain more HPM; if the fed funds rate moves below target, the system wants the Fed to drain some HPM through bond sales. Hence, the short term government "borrowing" rate will be administered through central bank targeting of the fend funds (overnight) rate.

Note that I do not deny that government's ability to sell government bonds (in other words, to substitute interest-earning bonds for non-interest earning HPM) might be somewhat interest rate sensitive. At a low interest rate, many of those with HPM might prefer to remain fully liquid; at a high interest rate, most might prefer to hold government bonds over HPM. Another way of stating the same thing is to say that the banking and nonbanking public's "portfolio allocation" between HPM and interest-bearing government debt might be influenced by the Fed's overnight rate target. What I do deny, however, is that the government deficit places upward pressure on interest rates (the hoary crowding out argument). Indeed, unless government drains excess reserves that can result from deficit spending, the overnight rate will be driven toward zero. This is because excess HPM will always flow first to banks (any nonbank entities with excess HPM will deposit it into the banking systemㅡalthough in reality because government spends by crediting bank reserves, government spending does not directly increase HPM held by the nonbank public, but rather directly increases bank reserves). Banks with excess reserves offer them in the fed funds market, but find no biddersㅡhence the fed funds rate will be quickly driven toward zero. Of course, this is how the Bank of Japan keeps the overnight rate at zero in the presence of huge government deficits; all it needs to do is to keep some excess reserves in the system.

This makes clear that the process through which holders of excess 'liquidity' 'force' government to 'borrow' really has to do with the interest rate setting mechanism (as Aspromourgos's intuition told him, unfortunately, his faulty analysis led him astray as he searched for 'equilibrium' portfolio relations). If the government is happy with a zero-bid condition in the fed funds market, it can simply leave some excess reserves in the system. Again I would not deny that the public's appetite for HPM and government bonds might be interest rate sensitive, which could increase the ability of government to deficit spend and issue HPM and interest paying debt. In the real world, however, we have not seen a situation in which the post-Civil War US government has offered dollars to buy goods and services without drawing forth some goods and servicesㅡwhich indicates that the nongovernmental sector's desire to net hoard (HPM plus government bonds) has never been reached. Nor even in the recent case of Japan, with zero overnight rates and a deficit in excess of 8% of GDP, has such a limit ever been reached. While such a limit might be a theoretically interesting constraint, apparently it is not a practical constraint. Nor is the theoretical constraint determined by "unused taxing authority" but rather by the nongovernment sector's desire to hold a combination of non-interest earning HPM and interest-earning bills and bonds.

6. Coordination and Consolidation of Treasury and Central Bank Balance Sheets

Some might argue that this is still too simple, and bring in the technical details of coordination between the central bank and the treasury. For example, Lavoie (2000) makes a distinction between the "neo-chartalist" and what he calles the "post chartalist" positions, the first of which applies to a nation in which the treasury spends by drawing upon accounts at the central bank (hence, government spending directly increases bank reserves) while the second applies to nations in which the treasury spends by writing checks drawn on private banks. According to Lavoie, this is an important distinction because in the neo-chartalist system it is true that the government spends first and then borrows, while in a post-chartalist system it is true that the government first issues debt held as an asset by private banks, which then create deposit accounts on which the treasury draws. Most importantly, Lavoie argues that the US and Euro systems are actually post chartalist, not neo-chartalist, precisely because both the Fed and the European Central Bank are prohibited by law from buying government debt directly from their national treasuries.

Actually,

the detailed coordination between the Fed and the US Treasury is examined in both my book and in Bell (2000), and there is no need to develop a separate "post" chartalist theory to deal with operating rules developed to minimize the "reserve effect" that results from fiscal operations. It is clear that the Fed and Treasury have developed their procedure to avoid the huge fluctuations of reserves that would otherwise result from timing mismatches between receipt of tax payments and emission of Treasury checks and their deposits in private banks. In reality almost all US federal government spending takes the form of writing checks on the Fed, and when these are deposited at private banks, reserves are increased. It is true that the Treasury engages in "advance selling" of bonds to Special Depositories, but this is not undertaken to provide "funds" to the Treasury so that it might spend; rather this is done in anticipation that reserves will be withdrawn soon through a tax and loan call (that drains reserves from Special Depositories). As Bell argues: " "It is impossible to perfectly balance (in timing and amount) the government's receipts with its expenditures. The best the Treasury and the Fed can do is to compare ^estimates^ of ^anticipated^ changes in the Treasury's account at the Fed and to transfer approximately the correct amount to/from tax and loan accounts. Errors due to excessive or insufficient tax and loan calls are the norm. ... When the Treasury is unable to correct these errors on its own, the Federal Reserve may have to offset changes in the Treasury's closing balance." (Bell 2000, p. 616) This is done through open market and discount window operations. While we don't have the space to go through all of these coordinating activities, it should be clear that all of this is monetary policy and has to do with maintaining stable fed funds rates, while it has nothing to do with fiscal operations. Hence, Lavoie's distinction between neo- and post chartalist is not helpfulㅡin either case, bond sales are an interest rate maintenance operation and not a financing operation.

The perceptive reader will object that there is indeed a financial constraint on government's ability to deficit spend: the inflation barrier. This is mostly correct. In a strictly technical sense, even if the inflation barrier is reached, government can still 'finance' its deficit spending so long as anyone will deliver goods and services in exchange for HPM. Still, the government might find that it is unable to increase real purchases because its additional spending only causes wages and prices to riseㅡwhat Keynes defined as "true inflation" : "When a further increase in the quantity of effective demand produces no further increase in output and entirely spends itself on an increase in the cost-unit fully proportionate to the increase in effective demand. ... " (Keynes 1964, p. 303) Thus, the inflation barrier is more properly thought of as a real constraint (full employment barrier) than a financial constraint, although at high enough (hyper-) inflation, the government might find nothing for sale for HPMㅡthat is, when the entire monetary system breaks down.

7. Horizontal Money and Neo-Chartalism

There has been some concern that the neo-Chartalist approach is not consistent with the Post Keynesian horizotal approach, or, at least, that I have not achieved a successful integration. Aspromourgos (2000, p. 144) claims my attempt to integrate the two (primarily in Chapter 5 of my book) "is not very helpful". While Mehrling did appreciate the "soybean futures parable of money" presented in that chapter, he has several complaints. First, he argues that consolidating the balance sheets of the Treasury and Fed obscures the difference between "money" and "state finance". Instead, he would keep them separate and would treat government-issued currency as a liability of the central bank rather than as an outside asset. In his view, "state money is not a fiat outside money...but, rather, an inside credit money because it is the liability of the central bank". (Mehrling 200, p. 405) This appears to be quite incorrectㅡthe central bank is no more 'inside' than is the treasury, which is why the private sector uses HPM for net clearing. Further, while hi is not explicit, his statement seems to suggest that he rejects the horizontal approach, which insists that the central bank has no separate discretionary power over its balance sheet. Mehrling proposes to treat HPM as "the liability of the central bank", or "as promise to pay". But, as discussed above, for what is the central bank liable, or, what does the central bank promise to pay? It only promises to accept its 'liabilities' in payments made to itself or to the state. Mehrling seems to imagine that the central bank 'promises' to pay foreign currencies, but this is true only on a fixed exchange rate systemㅡand even there it is only partially true. He also claims that "Wray's state theory of money ... Exists in {sic?} resolved tension with his nascent theory of money as nothing more than the open interest in fiat money." [n12] (Mehrling 2000, p. 405) He seems to believe that I view banks as "purely intermediary", which if true would require that I now reject everything I have previously written on endogenous money. [n13] (Wray 1990, 1992) However, Mehrling goes on, arguing "Viewing the bank money supply as the open interest in currency tends to shift our attention away from reserve requirements and money multipliers, and forces us instead to confront head-on the credit character of modern money, and its consequence." This does seem to recognize the "horizontal" nature of bank money.

Most Post Keynesians accept the horizontal view of central bank provision of reservesㅡif the central bank operates with an overnight interest rate target, it has no choice but to supply reserves on demand for otherwise the overnight rate would be pushed or pulled away from target. ( ... ... )

CF. tally stick

CF. tally stick