자료: Federal Reserve Bank of Richmond, Economic Quarterly, Volume 79/3 Summer 1993

※ 발췌:

The leading source of data on credit aggregates is the Flow of Funds Accounts (FOFA). This article provides an introduction to the accounts.

- The first section describes the nature, history, and availability of the accounts.

- Section 2 explains the accounts’ organization by sector and transaction.

- The third section traces the behavior over time of various credit measures from the FOFA.

- Section 4 highlights features of the accounts that warrant caution, and finally

- Section 5 provides suggestions for additional readings that provide a more thorough discussion of the accounts.

(...)

2. STRUCTURE OF THE ACCOUNTS

The FOFA are organized along two dimensions: by economic sector and by transaction type. The FOFA partition the economy into financial and nonfinancial sectors. The nonfinancial sector is then divided further into three categories: Private Domestic Nonfinancial, U.S. Government, and Foreign. Thus, the FOFA split the economy into four broad sectors:

- Financial,

- Private Domestic Nonfinancial,

- U.S. Government, and

- Foreign.

- Consumer,

- Business,

- Government, and

- Foreign.

The FOFA also are organized by the types of transactions among these sectors.

- Financial claims, such as demand deposits, bonds, corporate equities, and mortgages, represent different financial transaction categories.

- Nonfinancial capital transactions, which consist of saving and investment flows, constitute another transaction category. Estimates of the nonfinancial capital flows come directly from the NIPA.

Data on income, transfer payments, and expenditures on goods and services, are not included in the FOFA, except to the extent that saving is the balance of current receipts less current outlays.

In addition to being organized along those two dimensions, the FOFA also report data in two different but related ways:

- for stocks of financial assets and liabilities and

- for financial and nonfinancial capital flows.

For each sector, the reported stocks provide a balance sheet of the financial assets and liabilities of that sector. The reported flows record the change in balance sheet holdings of financial assets and liabilities between the current period and the previous one. The flow data also report nonfinancial capital transactions from the NIPA.

A. Sectors

Figure 1 shows the level of credit market debt owed by each sector from 1952:1 to 1993:1. Descriptions of each sector follow.

(1) Private Domestic Nonfinancial Sector

_ (1.1) Households.

_ (1.2) Nonfinancial Business

_ (1.3) State and Local Governments.

(2) Foreign

(3) U.S. Government : The U.S. government sector includes the activities of all agencies that are part of the budget of the United States and all off-budget activities, with the exception of certain financial activities. The Federal Reserve System is not included in this sector, nor are certain Treasury accounts related to monetary policy. Also, some federally sponsored credit agencies are not considered part of the United States government sector. Specifically, the financial sector includes the activities of the Federal Home Loan Banks, Federal Home Loan Mortgage Corporation, Federal National Mortgage Association, Federal Land Banks, Federal Intermediate Credit Banks, and Banks for Cooperatives.

(4) Financial Sector

_ (4.1) Federally Sponsored Credit Agencies and Federally Sponsored Mortgage Pools.

Federally sponsored credit agencies are considered private financial institutions despite their close legal association with the federal government. These institutions typically engage in very specific lending activities (e.g., the making of residential mortgages and farm loans). Federally sponsored mortgage pools include the Government National Mortgage Corporation, the Federal Home Loan Mortgage Corporation, and the Farmers Home Administration. These agencies raise funds by issuing securities that are backed by a pool of mortgages.

_ (4.2) Monetary Authority.

This sector includes the Federal Reserve System and certain Treasury accounts related to the conduct of monetary policy.

_ (4.3) Commercial Banking.

The commercial banking sector includes all banks that have head offices in the 50 states, U.S. branches of foreign banks, Edge Act and agreement corporations, U.S. agencies of foreign banks, bank holding companies, and banks in U.S. territories and possessions.

_ (4.4) Private Nonbank Finance.

Private nonbank finance includes all private financial institutions that are not part of the commercial banking sector. Included in this sector are deposit-taking firms such as savings and loan associations, mutual savings banks, and credit unions. In addition, insurance companies, private pension funds, state and local government employee retirement funds, finance companies, real estate investment trusts, money market and other mutual funds, and securities brokers and dealers are among those counted in this sector.

B. Transaction Categories

The FOFA are also organized by transaction categories.

- Transaction categories are broadly divided into two subcategories: nonfinancial and financial.

- The nonfinancial subcategory includes current transactions and capital transactions.

- In the FOFA, current transactions are summarized by total saving for each sector as in the NIPA, where saving is defined as the excess of current receipts over current outlays.

- Saving then enters as a source of funds for each sector in the capital account.

- Investment expenditures are the other half of the capital account.

- Financial transactions account for the remainder of the transactions in the FOFA.

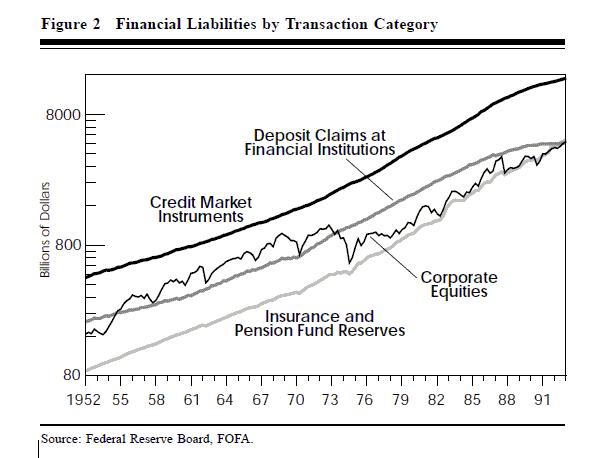

Financial Transaction Categories

(1) Monetary Reserves.

Monetary reserves are financial assets that can be used for intervention in foreign exchange markets by monetary authorities and for settlement of international transactions. The primary financial instruments included in this transactions category are gold, foreign currencies, and special drawing rights (SDRs). Transactions in these instruments occur among the U.S. government, monetary authorities, and the foreign sector.

(2) Insurance and Pension Fund Reserves.

Financial assets held by insurance companies and pension plans for payment of claims to household beneficiaries are included in this category.

(3) Net Interbank Claims.

Interbank claims involve transactions occurring between depository institutions and either the Federal Reserve or the foreign sector.

- Loans by the Federal Reserve to member banks, as well as depository institution reserves and vault cash held at the Federal Reserve, are included in this category.

- Federal funds and security repurchase agreements, however, are not included.

(4) Deposit Claims on Financial Institutions.

Deposit claims can be held in a number of different forms, including demand deposits, time deposits, federal funds, and money market fund shares. In all instances, the deposit claim is a liability of the financial institution receiving the funds and an asset of the individual or institution that lends or deposits the money.

(5) Credit Market Instruments.

Credit market instruments represent the primary source of funds to the nonfinancial sector. Instances of both direct and indirect finance are included in this category.

- One example of direct finance occurs when corporations issue bonds directly to the nonfinancial sector.

- The auctioning of U.S. government securities to private firms is another example of direct finance.

- Home mortgages, on the other hand, are an example of indirect finance where funds flow through the financial sector; mortgages are typically issued by a financial company using money that has been deposited with the institution by the nonfinancial sector.

(6) Corporate Equities.

Corporate equities are not debt. Instead, equities represent claims of ownership on a corporation. Unlike the treatment of most other financial instruments in the FOFA, equity issues are considered an asset of the holder, but not a liability of the issuer.

(7) Other Claims.

Any financial transaction that is not included in any transaction category described above is included in the “other claims” category. Security credit, trade credit, and equity in noncorporate business are among the items included in this category.

(...)

5. SUGGESTIONS FOR FURTHER READING

Much has been written about the FOFA. The following articles and publications provide additional guidance in understanding the FOFA.

The Federal Reserve Board’s Guide to the Flow of Funds Accounts provides a complete overview of the accounts. Particularly important is its discussion of the various sectors and transaction categories. This publication also provides, in line-by-line detail, a description of the source and/or construction of each data series. Additionally, it presents the accounting identities that constrain the FOFA using a matrix representation of the FOFA system. It also analyzes the movement of the data over time.

Wilson, Freund, Yohn, and Lederer in “Measuring Household Saving: Recent Experience from the Flow-of-Funds Perspective” furnish an excellent analysis of the gap between the NIPA and FOFA measures of personal saving in their discussion of the growing household sector discrepancy.

Hooker and Wilson in “A Reconciliation of Flow of Funds and Commerce Department Statistics on U.S. International Transactions and Foreign Investment Position” explain the differences between the international transactions statistics reported in the FOFA and the Commerce Department’s Balance of Payments Statistics.

Finally, Ritter’s “The Flow of Funds Accounts: A Framework for Financial Analysis” and Van Horne’s “Flow-of-Funds Analysis” detail the theoretical background for the accounts’ construction.

댓글 없음:

댓글 쓰기